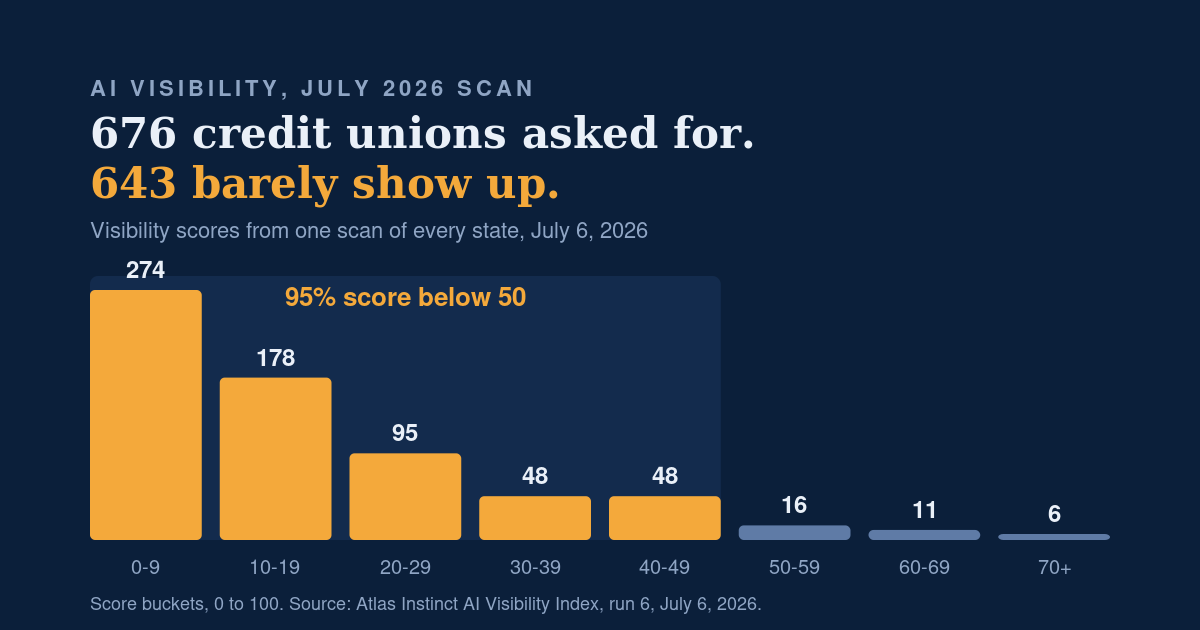

I asked an AI model where to bank in all 50 states and scored the 676 credit unions that came back. The national average was 18.1 out of 100, more than 95 percent landed below 50, and the two largest credit unions in the country both got beaten in their own backyards.

I did not expect to feel bad for the biggest credit union in America. Then I read the Virginia results.

Here is what I did. Using the AI visibility audit platform I built for Atlas Instinct, I asked the plain question a real person asks a real assistant. Where should I open an account in Vermont, in Ohio, in California. Not “credit unions near me.” No SEO-speak. Just the question, one state at a time, all 50 plus DC, run enough times to smooth out the noise.

676 credit unions came back. I scored each one from 0 to 100 on how often it showed up and how high it landed when it did.

The national average was 18.1 out of 100. The median was 13.5, which tells you a handful of strong performers are pulling the average up, not a few stragglers dragging it down. And 95.1% of the 676 scored below 50.

If this were a test, the credit union movement would be retaking the class.

The famous names that lost at home

Low averages do not surprise me anymore. I have written before that brand equity does not predict AI visibility. What I did not have until now were the names.

Navy Federal Credit Union is the largest credit union in the country by assets. In its own home state of Virginia, it ranks second, with a score of 39. First place goes to Langley Federal Credit Union at 41, an institution a fraction of Navy Federal’s size that apparently did not get the memo about knowing its place. PenFed, another national name, sits 11th in Virginia with a score of 7. It shows up in roughly one answer out of six. In its home market.

North Carolina is harsher. State Employees’ Credit Union is the second largest credit union in the United States by assets. In its own state it ranks 15th, with a score of 3 and a 17% appearance rate. The model would rather point you to Coastal Credit Union (47) or Truliant (46), and neither is anywhere close to SECU in size.

Decades of brand building, billions in assets, branches on every corner, and the model shrugs. Being the biggest name in your state does not mean the AI knows you exist.

Meanwhile, in Vermont

The best numbers belong to the small states. Vermont leads the country with an average score of 32.6, ahead of New Hampshire (31.2), Alaska (29.0), Rhode Island (27.4), and Delaware (26.8). The bottom of the table reads like a roll call of the biggest media and finance markets in the country: Illinois (11.9), DC (12.7), Michigan (12.9), New Jersey (12.9), California (14.1).

The widest gap in the country is in Oregon. OnPoint Community Credit Union scores 77 with a 100% appearance rate. Every single time someone asks, OnPoint is in the answer. The next credit union in the state, SELCO Community, scores 37. That is a 40-point canyon between first and second place, in the same state, chasing the same members.

And the highest score in the highest-scoring state? Vermont Federal Credit Union in South Burlington, at 72, also in every answer. A credit union most people outside Vermont have never heard of is running the table while household names post single digits.

Why this keeps happening

It is not marketing budget. It is whether the model has something legible to work with. Clear product pages. Structured data. Information it can read and trust without guessing. That is what separates OnPoint from SELCO, and Vermont Federal from competitors with bigger balance sheets and thinner websites. Structure beats volume, it is still the highest-leverage fix on the table, and most institutions have not touched it.

Accessibility feeds the same machine. It is the weakest category across every audit I run, and it is foundational, not optional. If a screen reader cannot parse your rate page, neither can a model trying to pull a fact to hand back to a member. Fixing it is not glamorous. It is usually cheaper than the campaign that is not landing.

None of this means the models are replacing credit union marketers. The job is changing verbs. The work moves from writing copy nobody structures to structuring information nobody has organized yet. The judgment stays human. The thing the model reads does not.

Where this goes from here

This was the sixth scan I have run, and the first one I have published. It updates every month from here. I would rather a credit union catch a problem in August than hear about it from a member who could not find them in July. For your own institution, I still think quarterly is the right rhythm, not once a year.

The index now has a permanent home at Atlas Instinct: the AI Visibility Index for credit unions. What is free there, and what I have shared here, is the national picture, one featured state, and the finding that surprised me most. The full 50-state tables and institution-level scores are there if you want to see your own state.

If you run marketing, strategy, or digital for a credit union and you want to know where you land, take the 90-second self-check or reach out. I will tell you straight, whatever the number says. Even if you are in Virginia.

Based on the July 6, 2026 AI visibility scan of 676 credit unions across all 50 states and DC, conducted by Kevin Farley through Atlas Instinct.

FAQ

What is the AI Visibility Index for credit unions?

It is a monthly scan, run by Atlas Instinct, that asks an AI model with live web search where to bank in every US state plus DC, then scores every credit union that comes up from 0 to 100 based on how often it appears and how prominently it is positioned.

How is the visibility score calculated?

The score blends appearance frequency and prominence. A credit union that shows up in every relevant answer, near the top, scores high. One that rarely shows up, or shows up buried in a list, scores low.

Why do small states like Vermont outperform bigger markets?

Less competition for the answer slot is part of it, but the leading institutions in Vermont also have clearer, more structured websites than most of their competitors. Fewer candidates plus better structure produces the gap.

Where can I see my credit union’s full state ranking?

The complete 50-state tables and institution-level scores are available through Atlas Instinct. Request your state to see exactly where your institution and its competitors land.